Heading into the second half of 2017, we believe the elongated U.S. credit and business cycle – currently eight years old and counting – will continue through the end of the year. Yet for the first time in almost a decade, the risks to the global economy are centered in the U.S. and not in other major world economies.

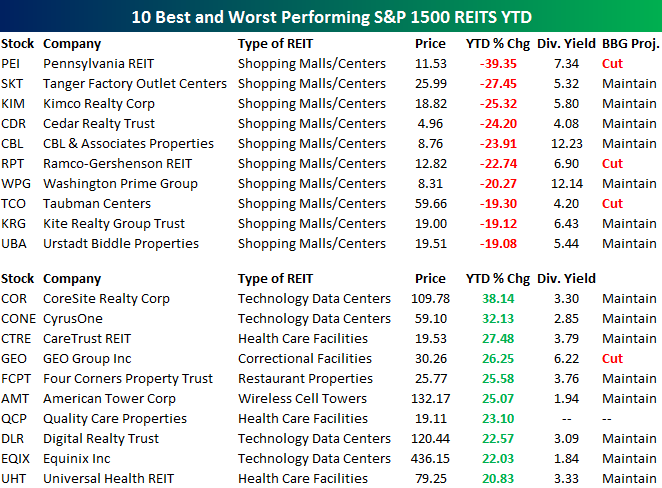

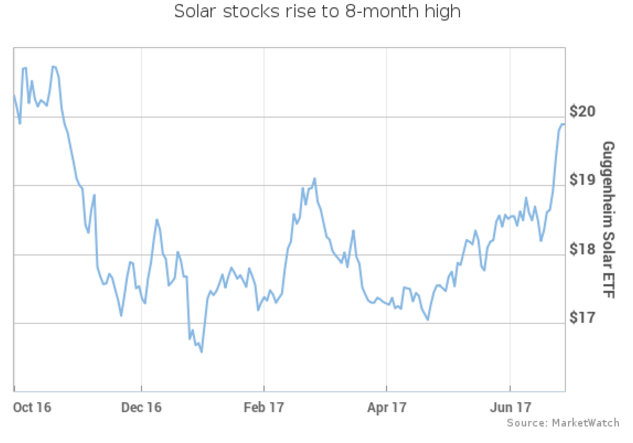

Growth in much of the rest of the world is stable or accelerating. In Europe, a much-anticipated credit and earnings cycle is underway, while most emerging markets are recovering from their 2015-2016 slowdowns and recessions. In our view, the biggest threat to the global economy is the prospect of the U.S. Federal Reserve (Fed) further tightening U.S. monetary policy. Against this backdrop, we believe: · Equities remain the asset class of choice. International equities are more attractively valued than, and likely to outperform, U.S. stocks. · Within the U.S., we favor growth companies in an environment where macro growth will continue to be scarce. · Long-term Treasury rates will remain low for the foreseeable future and send a message to the Fed to proceed with caution. · Emerging market sovereign and corporate bonds offer the most attractive value in fixed income for global bond investors seeking potential total returns. Market cycles ultimately end with tighter monetary policy and the yield curve inverting. We believe this time will be no different. Mutual funds are subject to market risk and volatility. Shares may gain or lose value. Foreign investments may be volatile and involve additional expenses and special risks, including currency fluctuations, foreign taxes, regulatory and geopolitical risks. These views represent the opinions of OppenheimerFunds, Inc. and are not intended as investment advice or to predict or depict the performance of any investment. These views are as of the publication date, and are subject to change based on subsequent developments. Carefully consider fund investment objectives, risks, charges, and expenses. Visit oppenheimerfunds.com or call your advisor for a prospectus with this and other fund information. Read it carefully before investing.  It’s beginning to feel like a summer lull out there for markets. But a herd of Fed speakers — including Janet Yellen — could break the pre-holiday spell and deliver a last-minute shake-up as this year’s first half wraps up today. Stocks don’t necessarily deserve a boost, with the Dow and S&P on track for their best first half in four years. And the NASDAQ is flirting with its biggest gain since 2003 (though techs don’t look too frisky in the early going). So, where to invest for the second half? Well, there’s lots of chatter about real estate investment trusts, aka REITs, after yesterday’s news that Warren Buffett has taken a big stake in Store Capital STOR, +0.71%. REITs can yield big profits — but only if you know which ones to buy, say Bespoke Investment Group analysts for our call of the day. “While the shopping mall REITs have been tanking, the REITs that lease out warehouses to tech companies that need space to house all of their servers and cloud data have been surging,” Bespoke’s team says. “The ten best-performing REITs in 2017 are all in strong uptrends, with the exception of GEO and QCP. If you’re a trend investor, you’ll like these charts,” the analysts add. (They’re referring to Geo Group GEO, -0.65% and Quality Care Properties QCP, +2.77 %.)  In other words, tech-exposed and health-care real-estate stocks have had a stellar start to the year and are likely to keep going up. Traditional retail real estate such as malls, however, faces “Death by Amazon” as shoppers shift online. That means investors should avoid that type of building, according to Bespoke. “While there has been lots of brainstorming about what to do with malls that often look like ghost towns these days, we haven’t seen any convincing ideas yet (except maybe turning them into tech data centers!),” the analysts say. One of Bespoke’s picks also gets praise from Forbes and Seeking Alpha scribe Brad Thomas, who singles out CareTrust CTRE, +0.57% as a “REIT gem” set for relatively speedy earnings growth. As for Buffett’s REIT pick, that’s along the lines of what Bespoke is backing — less than 20% of Store’s portfolio is in traditional retail. Key market gauges Dow ESU7, -0.34% and S&P futures ESU7, -0.34% are slightly lower, while Nasdaq-100 ESU7, -0.34% futures YMU7, -0.26% are showing a bigger loss. The dollar index DXY, -0.02% is suffering, largely because a jump in the euro. The shared currency EURUSD, +0.0000% surged to a two-week high after hawkish noises from ECB boss Mario Draghi. That drove European stocks SXXP, +0.60% lower. Crude US: CLU7 continues to recover and is taking a stab at reclaiming the $44 level, while gold US: GCQ7 is recovering from its “flash crash” yesterday. The chart The sun is shining again on shares of solar-panel makers, which have been through a rough patch. Now they’re rallying, after President Donald Trump said last week he wanted to clad the long-promised border wall with solar panels, to help pay for it by generating power. That helped send the Guggenheim Solar ETF TAN, +1.01% up 8% last week — the best weekly gain since December 2015 — and it continued to rise on Monday. That means it’s now trading at an eight-month high, as this chart shows. Analysts don’t necessarily believe the wall-plus-panels will see the light of day. But it’s a positive development that Trump’s making a pro-solar statement, they noted, according to The Wall Street Journal.  The buzz

Alphabet GOOG, -0.21% GOOGL, -0.34% is getting squeezed today after the EU’s antitrust body slapped the Google parent with a record €2.42 billion fine. Sprint S, +0.24% , Charter Communications CHTR, -1.52% and Comcast CMCSA, +1.11% are said to be in talks to bolster their wireless services. Pandora Media shares P, -1.66% is halted this morning and the rumor mill is going nuts. GM GM, +2.24% are waving another red flag for the car industry, warning its U.S. auto sales will fall short of forecasts. China’s Premier Li is touting the country’s “unimaginable job growth” at the annual June meeting of the World Economic Forum, which started Tuesday. All sorts of investing views have been getting shared at the Evidence-Based Investing Conference (West) The economy The flurry of Fed talk continues today, with Philly Fed’s Patrick Harker and Minneapolis Fed’s Neel Kashkari on tap. The highlight though is Chairwoman Yellen’s speech in London around lunchtime. On the economic docket this morning are the Case-Shiller U.S. home price index and the consumer-confidence index. See MarketWatch’s Economic Calendar. The quote “If, however, Mr. Assad conducts another mass murder attack using chemical weapons, he and his military will pay a heavy price.” — The White House accuses the Syrian government of preparing to use chemical weapons on civilians, including children. The stat 710% — that’s where Venezuela’s annual inflation rate stands, as the country battles with an ever deepening economic crisis. Professor Steve Hanke from Johns Hopkins University points out that it’s the first time inflation has spiked above 700% in the country since June 2015. Bob Ravnaas raised a paddle in a Houston auction house to secure his first block of mineral rights 19 years ago, when oil prices were swooning below $20 a barrel.

A generation later, that same West Texas oilfield is still spinning off royalties, part of a mineral-rights empire amassed by Ravnaas that stretches across 20 states and delivers millions of dollars in cash payments. Kimbell Royalty Partners LP, where the former petroleum engineer is now chief executive officer has stakes in 48,000 oil and natural-gas wells in some of the hottest U.S. shale patches. These days, it’s not alone. America’s drilling boom is making a hot commodity out of one of the stodgiest of oilfield assets, the monthly royalty check. Lured by the promise of steady returns without the cost of actually operating wells, companies like Kimbell are racing to acquire rights around the U.S. Private-equity giants including EnCap Investments LP and Blackstone Group LP are getting into the game as well, pouring billions into the market. “It’s become a very attractive investment," said Ravnaas, whose Fort Worth, Texas, company went public in February with a $90 million offering. “Oil and gas production has increased dramatically in the last ten years, and the size of the royalty market is increasing exponentially along with it." Drillers have negotiated with landowners for decades to tap the reserves below their acreage. But mineral rights have taken on new value as advanced drilling techniques sparked a renaissance in oilfields across the U.S. The rights guarantee holders an upfront bonus when an operator decides to drill and a cut of revenues for each barrel sold thereafter. Generational Turnover The growth in interest has been fueled by generational turnover. As time has passed, mineral rights have been passed down and diluted among successive generations. Descendants now see better value in packaging and selling off those rights for an upfront payment or equity in the new minerals companies, Ravnaas said. In what was once a mom-and-pop business, $20 million deals with Texas cattle ranches or other major landowners have become more common, according to the CEO. Speculators are knocking on doors and blanketing mailboxes in hot shale plays, hoping to amass mineral rights for cheap before the drilling companies arrive. Royalties typically range from an eighth of the per-barrel price to as high as a quarter in coveted areas like the Permian shale basin in Texas and New Mexico. Rights-holders aren’t on the hook for operating or financing costs to run the wells, although their income does depend on a driller’s willingness to keep pumping. Crude futures have fallen 14 percent in New York this year and were at $46.53 a barrel as of 10:06 a.m. on Friday. “It’s effectively a zero-cost exposure to the minerals" said Brian Brungardt, a Stifel Nicolaus & Co. analyst in St. Louis. He tracks Kimbell and two other royalty-chasing partnerships, Black Stone Minerals LP (no relation to the equity firm) and Viper Energy Partners LP. 20 Million Acres Collectively, the companies have spent more than $120 million to acquire new rights this year and now hold a claim on oil and gas royalties from more than 20 million acres in the Permian, Bakken, Marcellus and other shale fields, according to corporate filings. Private equity firms have jumped in as well, seeing mineral rights as a more affordable entree into the U.S. shale boom. In the Permian, drilling rights have reached $40,000 an acre and higher in the past year. The top price for mineral rights in the area is closer to $20,000 an acre, although competition has been pushing the tab up, said Rich Aube, co-president of New York-based Pine Brook Partners. The firm has devoted more than $100 million to royalty investments, including Brigham Minerals LLC. “It’s a new way to invest in the same resources in a way that’s less capital-intensive," Aube said in a telephone interview. “You have a lot of folks who want exposure to these resources with a different risk profile and have found this more attractively priced." Encap, Blackstone Houston-based EnCap, among the biggest energy-focused buyout firms, has devoted $1 billion to mineral investments, while New York-based Blackstone has invested more than a half-billion dollars. Aube said he knew of at least a dozen other equity firms that have assembled their own minerals teams. Representatives at EnCap and Blackstone declined to comment. The firms are pitching mineral rights as a new asset class for investors seeking better returns in a world of ultra-low interest rates. Viper Energy and Black Stone Minerals pay quarterly distributions that yielded more than 7.2 percent apiece as of this week, while Kimbell’s yield was projected at 5.6 percent, according to data compiled by Bloomberg. Each beats the average investment-grade energy bond yield of about 3.5 percent, according to Bloomberg Barclays index data. “You’ve got hundreds and hundreds of landmen that are constantly putting together an acre here and an acre there and then selling," said R. Davis Ravnaas, Kimbell’s chief financial officer and the CEO’s son. “We meet a new team almost every week." The risk for royalty collectors is that they’re at the mercy of a third party -- oil companies -- to keep the petroleum pumping. Kimbell reported a net loss in each of the last three years, after more than $40 million in writedowns related to slumping oil and gas prices. Despite those paper losses, cash flow and production continued to grow, the company said in an emailed statement. Kimbell credited “a highly tuned acquisition strategy which focuses on only buying high quality properties with ongoing development and upside potential." The market’s volatility puts a premium on having the right executive team, said Brungardt, the Stifel analyst. “You need a team in place that has got the experience in not only analyzing reserves and well economics but also the acquisition side," he said. “You may be sitting on a lot of acreage, but if nobody’s interested in it, you are out of luck." “It’s critically important to purchase not only the right rocks but the right rocks operated by the right operators," added Aube, of Pine Brook Partners. “You don’t control the pace of drilling, but that’s a judgement that affects the value of your asset and what your cash flow is going to look like over time.”  It's a question that vexes many mutual fund investors once they buy into the concept of investing through a Systematic Investment Plan (SIP): When you have a lump sum to invest, then over what period should you spread the SIP? Of course, for most SIP investments, the question does not arise. The most common type of SIP investment is a monthly one that goes out of a monthly income. This sort of SIP continues and is useful in a way to keep investing without bothering to actually take the time out and do it.

However, occasionally, the SIP investor gets a large sum of money at one go. It could be a bonus from a workplace, or it could be proceeds from the sale of some asset like real estate, or it could even be your retirement kitty which you need to spread and make it last for the rest of your life. Investing in an equity-backed mutual fund is the best way to get great returns over a long period like 5-7 years or more. However, over shorter periods, equity funds are dangerous. And when you invest at a large sum at one shot, then the risk is the highest. If the markets turn turtle, you could lose 10, 20 or even higher percentage of your invested amount very quickly. Since the beginning of the Sensex in April 1979, of the almost 13,900 possible six month periods, as many as 2,269 yielded a loss worse than 20%. If you just happened to catch a period like that at the beginning, then you would lose a large chunk of your capital right before it even starts growing. In theory, you could eventually recover, but in practice you would probably panic and pull out your money, making your loss permanent. The antidote to this is a Systematic Investment Plan. Spread your investment at a monthly periodicity over a certain period. Your entry price will be averaged out and you will be saved from the risk of a sudden decline. Moreover, you will end up buying more units of the fund when the markets are lower, which will enhance the returns you will get. That is of course, the standard set of advantages that a SIP has. However, the vexing question is what is this 'certain period'? Is it six months? One year? Two years? Or even longer? There are arguments for and against. Last week, I wrote about the research project on historic SIP returns that Value Research has carried out and we saw how SIP was truly safe for about four years and above. In this study, we found that on an average, if you invest in a SIP over four years, then your risk of a loss is negligible. It's also interesting that the risk of loss and the chance of an outside gain are both higher over short periods. Over longer periods, the good times and the bad get averaged out minima and the maxima converge. Consider this, for a typical fund with a multi-decade history, over all possible one year periods; the maximum returns are 160% and the minimum - 57%. Over two years, this becomes 82% and -34%. Over three, 63% and -18%. Over five, 54% and 4%, meaning never any loss. Over ten years, maximum is 30% and minimum 13% .These is all annualized figures. The trade-off is crystal clear--the shorter the period, the higher the potential gain but the worse the possible risk. The answer from this data appears to be that SIPs must last more than three years. If you seek zero risk of loss, then that is the correct answer. However, for many investments, this is too long. If you are getting an annual bonus from your employer, it would be ridiculous to spread it over 3-4 years. If you have sold some ancestral property and the sum realized will be the core of your old age income, then you need to be cautious about the risk you take. In a case like this, you would do well to forego some potential income to ensure that you don't make a loss. A rule of thumb is that you could invest the money over half the period that it has taken you to earn it, subject to the maximum of 4-5 years. So annual bonus could be invested in six months, while ancestral property could take five years. It's basically a way of linking risk to how significant that sum of money is for you.  Buying stock is easy. The challenging part is choosing companies that consistently beat the market.

That’s something most people can’t do, which is why investing in a diversified mix of low-cost index funds and exchange-traded funds is a smart long-term strategy for the average investor. So smart that even diehard stock jocks swear by indexing for the money they’re not using to buy individual equities. But you’re reading this to get better at investing in stocks. We’ll assume you’ve got a yen for research, time to let your investments ride through many market cycles and have set parameters for the amount of money you’ll put on the line. (We recommend no more than 10% of your overall holdings be invested in individual stocks.) And let’s not forget this vitally important investing PSA: “Money you need in the next five years should not be invested in stocks.” Here are five investing habits essential for success in the stock market: · Check your emotions at the door. · Pick companies, not ticker symbols. · Plan ahead for panicky times. · Build up your positions with a minimum of risk. · Avoid trading overactivity. 1. Check your emotions at the door “Success in investing doesn’t correlate with IQ … what you need is the temperament to control the urges that get other people into trouble in investing.” That’s wisdom from Warren Buffett, chairman of Berkshire Hathaway, oft-quoted investing sage and role model for investors seeking long-term, market-beating, wealth-building returns. Buffett is referring to investors who let their heads, not their guts, drive their investing decisions. In fact, trading overactivity triggered by emotions is one of the most common ways investors hurt their own portfolio returns. All the investing tips that follow can help investors cultivate the temperament required for long-term success. 2. Pick companies, not ticker symbols It’s easy to forget that behind the alphabet soup of stock quotes crawling along the bottom of every CNBC broadcast is an actual business. But don’t let stock picking become an abstract concept. Remember: Buying a share of a company’s stock makes you a part owner of that business. You’ll come across an overwhelming amount of information as you screen potential business partners. But it’s easier to home in on the right stuff when wearing a “business buyer” hat. You want to know how this company operates, its place in the overall industry, its competitors, its long-term prospects and whether it brings something new to the portfolio of businesses you already own. 3. Plan ahead for panicky times All investors are sometimes tempted to change their relationship statuses with their stocks. But making heat-of-the-moment decisions can lead to the classic investing gaffe: buying high and selling low. Here’s where journaling helps. (That’s right, investor: journaling. Chamomile tea is a nice touch, but it’s completely optional.) Write down what makes every stock in your portfolio worthy of a commitment and, while your head is clear, the circumstances that would justify a breakup. For example: Why I’m buying: Spell out what you find attractive about the company and the opportunity you see for the future. What are your expectations? What metrics matter most and what milestones will you use to judge the company’s progress? Catalog the potential pitfalls and mark which ones would be game-changers and which would be signs of a temporary setback. What would make me sell: Sometimes there are good reasons to split up. For this part of your journal, compose an investing prenup that spells out what would drive you to sell the stock. We’re not talking about stock price movement, especially not short term, but fundamental changes to the business that affect its ability to grow over the long term. Some examples: The company loses a major customer, the CEO’s successor starts taking the business in a different direction, a major viable competitor emerges, or your investing thesis doesn’t pan out after a reasonable period of time. 4. Build up positions gradually Time, not timing, is an investor’s superpower. The most successful investors buy businesses because they expect to be rewarded — via share price appreciation, dividends, etc. — over years or even decades. That means you can take your time in buying, too. Here are three buying strategies that reduce your exposure to price volatility: Dollar-cost average: This sounds complicated, but it’s not. Dollar-cost averaging means investing a set amount of money at regular intervals, such as once per week or month. That set amount buys more shares when the stock price goes down and fewer shares when it rises, but overall, it evens out the average price you pay. Some online brokerage firms let investors set up an automated investing schedule. Buy in thirds: Like dollar-cost averaging, “buying in thirds” helps you avoid the morale-crushing experience of bumpy results right out of the gate. Divide the amount you want to invest by three and then, as the name implies, pick three separate points to buy shares. These can be at regular intervals (e.g., monthly or quarterly) or based on performance or company events. For example, you might buy shares before a product is released and put the next third of your money into play if it’s a hit — or divert the remaining money elsewhere if it’s not. Buy “the basket”: Can’t decide which of the companies in a particular industry will be the long-term winner? Buy ’em all! Buying a basket of stocks takes the pressure off picking “the one.” Having a stake in all the players that pass muster in your analysis means you won’t miss out if one takes off, and you can use gains from that winner to offset any losses. This strategy will also help you identify which company is “the one” so you can double down on your position if desired. 5. Avoid trading overactivity Checking in on your stocks once per quarter — such as when you receive quarterly reports — is plenty. But it’s hard not to keep a constant eye on the scoreboard. This can lead to overreacting to short-term events, focusing on share price instead of company value, and feeling like you need to do something when no action is warranted. When one of your stocks experiences a sharp price movement find out what triggered the event. Is your stock the victim of collateral damage from the market responding to an unrelated event? Has something changed in the underlying business of the company? Is it something that meaningfully affects your long-term outlook? Rarely is short-term noise (blaring headlines, temporary price fluctuations) relevant to how a well-chosen company performs over the long term. It’s how investors react to the noise that really matters. Here’s where that rational voice from calmer times — your investing journal — can serve as a guide to sticking it out during the inevitable ups and downs that come with investing in stocks.  According to David Fabian, “A vital part of Investment success depends upon one’s ability to compare historical returns with an index or benchmark.

Doing so will let you measure if your approach meets the performance expectations or evaluate the efficiency of somebody else’s recommendation prior to hiring them. Although is may be very common in the entire industry, many investors still make knee-jerk conclusions based on unreliable or biased information. Two primary conditions that must be satisfied when determining the viability of any investment approach are discussed below: A proper standard of evaluation We now lay down the reasons why these concepts are essential to your decision process. Let us talk about time. In reality, time is a commodity that has lost its overarching value in the fast-evolving dynamics of our daily existence. People so often fall prey to the temptation of immediate gratification provided by modern technology that they totally overlook how much time is required to accumulate wealth through the process of compounding. For instance, if you start saving and investing starting at your mid-20’s and then you retire in your mid-60, it would have taken you 40 years to accumulate your wealth. But it does not end there. You need to sustain your wealth’s security for another 20 years through managing and conserving your investable assets. The growth period alone will take 480 months or 40 years, while the distribution or income period could last for 240 months or 20 years more. You need enough patience to see it through. You cannot simply compare returns over very short time-durations. That is why you can hear people cry: My portfolio has been stagnant in four months! I’m below the benchmark on a 6-month rack record! Alas, my portfolio is 250 basis points lagging from the S&P 500 this year – I am done for! The truth is that even the most efficient investment method will suffer some setbacks through underperformance. It may take some months or even last for a couple of years or more at a time. The best step to take during such doubt-filled or self-pitying moments is to recall why you chose this strategy in the first place. Is your investment strategy still consistent with your risk tolerance level? Could there be an intervening and temporary factor that is causing the adverse conditions? Can you do something to manage this factor in order to enhance your long-term returns? Have you really considered the risks of shifting to another approach in mid-stream? Experts would advise that you analyze the performance of any investment method over a period of 3 to 5 years, enough time to determine the strengths and weaknesses over several conditions of the markets (bear, bull, transitional, and others). The bond or stock markets can proceed for a few years along a particular direction. While that may favor some investors, it can also hurt others. Not that either side is bad investing; it all has to do with each group being exposed to different risks. Creating and protecting your wealth is not a 100-meter dash -- a short-distance race, so to speak. Rather, it is a marathon -- a sustained race where risk conditions must be considered at close-range and behavioral principles applied with accuracy. Great patience is, therefore, of utmost importance in order to succeed as an investor. There are no short-cuts in this industry. A Suitable Benchmark A common pitfall among investors is the tendency to compare apples and oranges. A prime example is that of a company whose primary approach is to have a mix of bonds and stocks allocated through ETFs that are adjusted according to meticulously-developed strategies. As such, it has a total of 20 to 40% stocks and 50 to 70% bonds in the Strategic Income Portfolio at any particular period. However, the most common feedback the company derives when evaluating performance is how its portfolio stacks up against the S&P 500 Index. It seems that people are programmed to think that the S&P is the singlular reliable benchmark available, such that it has become the darling standard of many index lovers throughout the world. Obviously, there is no basic logic to comparing the returns of a 100% stock portfolio (the S&P 500) versus a multi-asset portfolio that contains less than 50% exposure in stocks. A better and more suitable benchmark for such a type of investing method would be the 40/60 allocation in the iShares Core Moderate Allocation ETF (AOM). That is where the data will exhibit a clearer picture of actual performance. In a similar manner, comparing the 0 to 60 mph rate of starting acceleration of a Porsche in a few seconds to that of a Suburban would not make sense either, would it? Although that is an accepted truth, in general, only a few investors consistently apply that universal principle in their investment practices. It is vital to appreciate that fundamental concept in the process of accurately measuring risks or comparing similar approaches. Never compare investing in bonds and stocks to the revenues of a CD or a money market account. Never relate a portfolio of technology stocks to closed-end funds. And never compare hedge-fund revenues to that of a bunch of ETFs. We can continue down the line. . . . Perhaps, the most difficult hurdle to making this logical conclusion is the fact that most investors do not know the suitable benchmark for comparison objectives or where to locate them. They merely gravitate to the S&P 500, the NASDAQ Composite or the Dow Jones Industrial Average because they see them flashed on the news or on the web daily. In the end, every particular asset type or investment instrument should be weighed or evaluated by a similar group of equals. ETFs have made that process less difficult for many years now; however, you must always undertake the task of finding an appropriate index to serve as a benchmark. Ask a professional analyst how and where to find a good benchmark as a reliable yardstick. The Ultimate Goal Investing involves a lot of psychology and comprehension of the relationship of certain facts and information. This article hopes to develop a new perspective not considered previously or to strengthen an existing point-of-view. It is hoped that either way, the reader will attain a more reliable and more solid frame of reference for evaluating a portfolio’s performance in the future.  As early as you can, avoid common mistakes so you can enhance your retirement savings without losing precious time.

Saving for your retirement while you are in your early twenties can be one of the wisest financial decisions you can make. This is proven by the fact that starting in your 20’s can help you gain hundreds of thousands of dollars more than if waited until you are in your 40’s. Nevertheless, deciding to save money may not always be a sure path toward financial success. You must be aware of certain errors most people are prone to commit along the way and which you must avoid in order to safeguard your future. Along with saving for retirement, you need to enhance your financial intelligence on the path to a secure future. So, even without consulting with a financial adviser and assessing your situation, these following tips will give you some general and practical advice on avoiding the common mistakes in saving for retirement. #1: Too Much Caution so Early in the Game Striking a healthy balance between caution and eagerness helps a lot; hence, do not be too cautious early in your plan. Starting at the age of 25 is ideal, as most experts say, gives you about 30 or 35 years prior to using your retirement savings. With still plenty of time in your hand, you can have the luxury of taking some chances instead of being too cautious. And so, investing into one or two big investments that early on in your career can provide substantial revenues within a long-term investment time-frame. On the other hand, you may go to the other extreme and take the extremely conservative approach, which may prevent huge losses but also keep you from significant returns. #2: No Diversification Avoid also the mistake of putting all your eggs into one basket, or into one asset type. Let us consider the stock market. Assuming you put your whole retirement portfolio into stocks and you gained a massive $1 million return over the years. At 59, with one year remaining until your planned retirement, the market suddenly falls and suffers losses of 40% and eating away $400,000 off the stock value. It would take short of a miracle to recover that huge loss within one year! The solution is to diversify. Balance your savings and choose more conservative investments in the few remaining years of your career. #3: Neglecting to Consider Fees Majority of people make the mistake of not taking the time to study the fees connected with retirement savings. One percentage point increment in fees could mean costs of up to tens of thousands of dollars over the entire duration of an account. Analyze fees like a bee searching for honey and avoid entering into an account without a thorough picture of the fees required. #4: Aimlessly Moving On Setting up retirement goals at the start beats having to proceed aimlessly, even though life is unpredictable and you will always experience such situations as salary reduction or other external economic factors. Having exact amounts to aim for and deciding when you need to enter into new investments will help you easily manage your finances, since you know where you are exactly at the scoreboard and how much time you have left. #5: Avail of Tax Breaks when Filing How to manage taxes well forms a big part in a successful retirement planning. Certain accounts will give you the option to defer tax payments until maturity, allowing your money to grow more with interest. Others demand that you pay post-tax payments, freeing you from having to pay when you withdraw the money. To know more on this matter, consult with a financial adviser to decipher the pros and cons of either of the two schemes. Be Wise: Plan Right and Avoid Retirement Mistakes The wise always plan ahead, enhancing the likelihood of securing a secure and comfortable retirement with sufficient money to support their needs over the coming golden years. The key is to avoid those mistakes that erode your portfolio’s full potential or stunt its growth. Commit yourself to these proven guidelines and rest easy knowing a bright future awaits you.  You must have taken a peek at this year’s billionaires who made it to the top of the list of those who added fortunes to their wealth. How many billions did they gain over the previous year’s figures?

Most investors think that having a high debt is undesirable and must be avoided. Naturally, they tend to see it as adding more risks to a company’s present exposures. And once that company defaults on its debts because of underperformance, it could fold up. Nevertheless, high debt can lead to positive consequences. It can bring in greater returns, even offsetting the greater risks involved in the process. Enhancing yields The major reason why debt can improve overall returns is because it costs much less than equity. A firm can raise capital either through equity or debt, with debt generally offering a less expensive option. Hence, maximizing a company’s debt levels in order to generate higher returns on equity is more logical. It can lead to greater profitability, stronger share-price performance and increased dividend growth. The proper circumstances Admittedly, maxing out a company’s debt levels is not a wise move at all times. Businesses with highly seasonal performance and dependent upon the conditions of the general economic environment might encounter great difficulties if their balance sheets are heavily leveraged. During times of low returns, they may not be able to undertake debt-servicing steps, aggravating the company’s situation. On the other hand, companies performing in sectors that offer strong, consistent and viable revenues should increase debt to comparatively higher levels to enhance the gains for their equity-holders. For instance, it is to the advantage of utility and tobacco firms to raise their debt levels because of their high level of earnings visibility and the relatively strong demand for their products. Economic periods During periods of low interest rates, it certainly makes sense for businesses to borrow as much as possible. The previous ten years provided such an opportune time to borrow, rather than to lend. Global interest rates have experienced such record lows, thus, leading many companies in various sectors to decrease their overall borrowing rates. In the future, a higher rate of inflation is expected, portending higher interest rates. Although it could lead to increases in the cost of servicing debt, it should be compensated somehow by higher prices passed on to the end consumer. Moreover, a higher inflation rate will serve to diminish the real-terms value of debt. This can lead to increased levels of borrowing in the future. Conclusion Although increasing debt levels can also increase overall risk, it can be a viable step under the proper conditions. During periods of low interest rates, businesses with strong business models may enhance overall revenues by raising debt levels. And while higher interest rates may entail rising costs of servicing debt in the future, higher inflation may reduce the real-terms value of debts. Hence, investors can opt to buy stocks with a modest degree of debt exposure to optimize their overall gains over the long-term.  What is the difference between investing money and saving money? Although they seem to be similar, they mean entirely different things. Knowing the difference and applying that knowledge can help you build your personal wealth.

So many novice investors do not realize the fact that the two have different uses and have distinctive roles in their financial approach and balance sheet. As you begin the adventure of enhancing your wealth and establishing financial freedom, learn how to avoid problems by properly dividing and allocating your money. A lot of individuals, in spite of having great portfolios, lost everything for not having given sufficient respect to cash in their portfolio. Cash has exceedingly greater use than merely for making more cash. To appreciate the use of cash, let us see how investing and saving differ. Defining what Saving Money Means The idea saving money involves keeping hard, cold cash in a secure place, as well in liquid (that is, easy to access or sell in a matter of days) assets. This includes checking accounts and guaranteed savings accounts. You can also include U.S. Treasury bills or money market accounts, although the latter involves a lot of monitoring work. Most of all, your cash funds should always be ready to use for your needs; available at any time for immediate withdrawal with the least delay under any circumstances. Most rich and famous investors, including veteran investors who went through the Great Depression, strongly recommend hiding plenty of cash in secret storages even if that will incur a big expense in terms of profit loss. Although the papers did not carry the news, back in the 2008-2009 market collapse, some hedge fund managers were apparently asking their spouses to withdraw as much cash as possible from ATMs, expecting the whole economy to collapse and limiting the availability of greenbacks for a short period.. After you have ascertained the preservation of your capital should you consider secondary measures for money you have kept in savings. That is, hedging against inflation. Defining What Investing Money Means Investing money involves using your money or capital to acquire an asset with the potential of producing a safe and reasonable rate of return, allowing you to build wealth even through volatile periods, which can run into years. Genuine investments have a certain factor of safety, usually in the form of assets or owner returns. From your basic lesson in novice investing, the most productive investments are such assets as bonds, stocks and real estate. What is the Desirable Ratio between Savings and Investments? As a rule, saving money should generally take precedence over investing money. Consider it as the foundation over which you will erect your financial house. For a very simple reason: Unless you have inherited a sizeable amount of wealth, your savings alone will generate the capital to support your investments. During the lean periods when you will need cash, chances are you will have to sell your investments at the most inopportune time. Such an event would set you back by a big stretch. Two major kinds of savings strategies should become part of your financial concern. They are: · As usually recommended by experts, your savings should be enough to address all your personal needs, such as food, mortgage, utility bills, loan payments, insurance costs and clothing expenses for a period of six months. Hence, in case you lose your job, you still have enough time to cope with the crisis without the daily stress of working for a regular salary. · Whatever specific goal in your life that will demand a big amount of cash for at least 5 years should be powered by savings, not by investments. In the short-term run, the stock market can be considerably volatile, taking away 50% of its value within a year. Buying a house can be a prime example for saving your money in real estate instead of investing it. With these things under your belt, you can acquire health insurance as your first line of defense in your portfolio. One possible exception is contributing to a 401(k) plan at your company in order to get free money from your employer’s matching contributions. That is on top of getting a large tax break for contributing to your retirement account. You also have material bankruptcy safeguards for assets held within such an account against any non-payment or default on your part. Additional Info on Saving Money Avail of more information on how you can start saving money by reading online materials for beginners on how to save money. Get hold of resources, articles, essays, and lessons teaching you how to save money, how to invest money and how to build your personal wealth. It may seem scary for now, but remember that even successful and rich people began by earning money, living within their means, saving money and investing in ventures that brought interest, dividends or rentals. You can be as good, if not better, than they are. It is all a matter of gaining the same knowledge and wisdom to allow you to act as prudently in handling your money with discipline in order to reap a certain measure of success. In the same way that they did their homework and applied the right principles of money management, saving your own money can be as simple as adding 1 and 1 to get 2.  If you are involved at present in a tussle with your life insurer over the escalating costs of their universal life premiums, you may need this article like a shot in the arm.

Within the past couple of years, scores of universal life insurance policyholders have been adversely affected by the double-digit premium increases from firms such as Axa Equitable, Transamerica and Voya Financial. And more premium increases, particularly to long-time policyholders, are still coming. Universal life was developed in the 1970s and accounted for one-fourth of all of life insurance policies bought from the ‘80s to the ‘90s. This development will affect tens of millions of people who will have to eventually deal with huge premium increases. What is Universal Life Insurance? What is happening? To fully understand, let us start from the beginning. If you are not familiar with universal life, it is a permanent (for as long as you pay the premiums promptly) and rather flexible, crossbreed life insurance policy that mixes the sensibly affordable properties of term insurance with a savings component similar to whole life insurance. A universal life insurance policy provides holders a “cash value” savings account that brings them tax-free interest, including the flexibility to modify premiums and to raise or reduce death benefits. The policy’s investment account earns cash when interest rates rise but can also deplete it when rates dip low, as in the present. During the ‘80s and the '90s, the most accepted guaranteed rate in universal life policies was 4%; although some insurers offered more, says James Hunt of Consumer Federation of America. Premium Increases of More than 200% In the past two years, numerous universal life policyholders have been warned that their insurers are hiding in the fine print of their contracts their option to substantially raise their long-steady monthly premiums. And so, more than a few customers have suffered hikes of more than 200%. It means that some people who are aged from 60 to 80 or more, many of whom receive fixed salaries, are being told to pay up amounts ranging from a few hundred dollars to thousands of additional dollars monthly for policies they bought many, many years back. The consequence of not doing so will be the lapse of their policy or the surrender of the policy and withdrawing any cash value remaining (with some possible taxes on that value). In any case, no death-benefit will be in sight. An 82-year-old retiree, Nicholas Vertullo of Long-Island, told The Wall Street Journal last August that his premiums for 3 universal life policies more than 200% hikes, reaching a staggering $30,000 yearly premiums (for a death-benefit of $500,000). And he had promptly paid premiums for about 3 decades. We wonder where all the goodwill in return for all the years of loyalty shown went. Why the Unimaginable Rise of Universal Life Premiums? How could this thing happen -- and why is it happening at all? It is because of the economy, according to life insurers. In the 1980s, interest rates gradually declined and suddenly plunged during the 2008 recession as the Federal Reserve took some measures to enhance the economic situation by providing easy access to borrowed money. However, low interest rates adversely affected majority of investors, life insurers included. This led to minimal returns for insurers who invested their money heavily. As a result, life insurers started protecting their investments and hiked premiums on policies bought in the not-so-recent past. (Many of the policies offered in recent years are tied to the stock market and offer no guaranteed returns of a minimum of 4%.) How Policyholders and Insurers Respond Justifiably, many universal life policyholders who got assurance that their premiums would remain fixed are not happy about all this development. According to The New York Times, a dozen lawsuits have been filed against insurers who had sold such policies. Feeling some pressure from public opinion, some insurers are said to have reimbursed, in part, some determined holders who had complained after they were being required to drop their policies. From the looks of it, there seems to be no positive outcome to this trend in the insurance sector. Safeguarding the Rights of Universal Life Policyholders Steps are being made by several regulators and consumer advocates to seek protection for universal life policyholders. A recent by the New York Department of Financial Services seeks to require insurers to inform the agency not more than 120 days before instituting any “adverse change” in “non-guaranteed elements of an in-force life insurance or annuity policy.” The rule likewise requires insurers to inform policyholders not more than 60 days before any change. The regulation may serve as a precedent regulation for other state insurance agencies. Moreover, in 2016, the Consumer Federation of America sent a letter to all state insurance commissioners requiring them to evaluate and prevent any unjust price hikes being implemented on holders of universal life policies. In case you are one of those who has an older universal life policy and have not experienced any premium hike, expect it to come soon. The better approach is to become proactive and find out ways to avoid being hit by an adverse increase. Recommendations for Longtime Universal Life Customers Be prepared by taking the following steps: · Get in touch with your insurer and ask the exact value of your policy’s cash reserves. Based on the amount you have accumulated from the start, you might be in a position to weather any premium hikes in the future. · As an alternative, try asking your insurer to reduce the policy’s death benefit, and subsequently, your premiums. · Ask if you can change your policies. Perhaps, they have other policies they can offer you. If you are in your 60s or more, however, it might be quite difficult to get approval for a life insurance policy. · Failing all else, find a life insurance firm or agent who could purchase your policy in exchange for getting the death benefit in the future. |

RSS フィード

RSS フィード