I find that the end of the year is always a good time to examine my investment portfolio and determine whether any changes need to be made. If some investments have performed well and distorted my asset allocation, it may be time to take some profits off the table and rebalance the portfolio. Similarly, if there are attractively valued sectors, stocks or countries that I am neglecting, I can look at adding exposure.

With that in mind, here’s a brief look at where I’ll be investing in 2018. Dividend stocks Dividend stocks currently make up around 75% of my portfolio. That’s something I won’t be changing in 2018. Dividend investing, while not the world’s most exciting investment strategy is one that works for me. One of my main investment goals is to build up a large dividend portfolio that pays me a sizeable income stream. I still have a long way to go; however, I’m hoping one day that dividend stream will be enough to live off. In 2018, I’ll definitely be looking to add to this section of my portfolio. The good news is that there’s plenty of value to be found in this area of the market right now. For example, stocks such as Lloyds Banking Group and Legal & General Group currently offer prospective yields of 6.2% and 5.7%, yet trade on P/E ratios of 8.4 and 10.6. At the same time, stocks that are considered to have highly dependable earnings such as Unilever, Diageo and Reckitt Benckiser currently trade at premium valuations. I’ll be keeping a close eye on these kinds of stocks in 2018, in the hope that a little market volatility throws up attractive entry points. Growth stocks Growth stocks make up the other 25% of my portfolio. This part of my portfolio has performed well in 2017 and several small-cap stocks I own have soared. Given their high valuations, I may take some profits off the table. I’ll continue to look for under-the-radar growth opportunities next year. However, I do think a little bit of caution is warranted towards growth stocks. Neil Woodford recently stated that the difference between the performance of US value stocks and growth stocks today is “greater than at any stage in stock market history”. Geographic mix The bulk of my portfolio is currently invested in UK stocks, although I do have funds that have exposure to North America and Europe. US equities have had a strong run this year, and the valuation of the S&P 500 now looks expensive in my view. The FAANG stocks have all rallied hard, with Amazon now trading on a P/E of 300. For this reason, I’ll be reducing my exposure to the US. From a long-term investment point of view, I really like the emerging markets. Countries such as China and India have compelling long-term growth potential. I feel that I need more exposure in my portfolio. However, the MSCI Emerging Markets index has risen over 30% in 2017. Therefore, it might be sensible to wait for a pull back before I invest.  Everyone knows you cannot hang a shingle and announce that you have started a business. Launching a company involves research, planning, financing, and fulfilling legal requirements. Starting a business involves planning, making key financial decisions, and completing a series of legal activities.

The way to put the best foot forward is by writing a business plan to that outlines the way that a company will reach its potential. Then, it comes time to set all the plans into motion. As the end of 2017 approaches, aspiring entrepreneurs will reassess their situations and consider taking the plunge into business ownership in 2018. It doesn't happen overnight. Rather, it is a process. 1. Conduct market research Before making any investments, conduct market research to determine if there really is an opportunity to turn the idea into a successful business. Gather information from potential customers and existing business owners in the surrounding area and then utilize the intelligence to develop a competitive advantage in the marketplace. 2. Write a business plan You can’t get somewhere without knowing what route you will take. That’s where a business plan comes into play. The business plan will outline what the business is, where it is located, who is running it, when it operates and how it will achieve a profit. A well written business plan is a vital step in the process of securing a small business loan. The most important element of the business plan will be the one-page Executive Summary at the beginning of the document. The summary should detail the name of the business, what product or service it will provide, the competitive landscape in the local market, the differentiator that will set the business apart from its competitors, the management team and each member’s experience in the industry, marketing plan, and financial projections. 3. Secure funding Once you figure out what is needed to run the business, draw up a budget so that you can figure out how much money you’ll need to start it. Some people will tap into their life savings to launch a new business. Others will call upon family and friends. Obviously, if you don’t have enough money or willing backers to self-finance the venture, a traditional bank loan or SBA loan may be the way to get the business off the ground. Currently, big banks are approving 25 percent of the small business loan applications that are submitted, while smaller banks are granting slightly less than half of the requests they receive. Before applying for a loan, check your credit rating. If it’s in the 700 to 800 range, lenders will be more likely to fund your venture than if you have a score of 650 or less. Be prepared to provide tax returns from the previous two or three years. Having a business plan is also an important document. All of this information will help build the case to a potential funder that your venture is a sound one and that you are likely to be able to pay the money back in a timely manner. 4. Pick a location Real estate agents always stress location, location, location. Picking the right location for a business is one of the most important decisions an entrepreneur will make. The choice will have a direct impact on your revenues, taxes, legal requirements and cost structures. A busy street is a great location for a restaurant – unless there is no place to park. Having great food and good pricing may not help if customers cannot find a place to park without getting a ticket. If you choose to open a nail salon in a town, be sure that there aren’t already 10 others in a one-mile radius. The local market may be saturated. Keep these things in mind when selecting a location. Price should not always be the deciding factor. 5. Choose a business structure Creating a formal, legal structure for your business provides legitimacy and has an impact on the amount you pay in taxes and the protection of your personal assets. Your attorney can help with the process. There also are a number of firms, such as Incorporate.com, which can assist in the formation of an LLC, C-Corp, S-Corp, or other type of business structure. 6. Get federal and state tax IDs Every company should establish a federal employer identification number (EIN). Without it, a business will be unable to open bank accounts or credit card accounts. It’s also necessary for paying taxes, which of course, is part of business ownership. 7. Apply for required licenses and permits Be sure that your company has all the necessary licenses and permits to operate in the location you have chosen. For instance, a restaurant could be required to have a vendor’s license from the town while the local health department may require passing a food hander's safety course. Once these seven steps are taken, a business is ready to cut the ribbon and ringing up sales. Be sure that you have established a business bank account for deposits and operational expenses and a payroll account to pay workers. Your local bank will gladly work with you to set up merchant services (credit card processing). Join the local chamber of commerce, which can be instrumental in supporting the start of a new member organization. An active chamber will be able to set up a ribbon-cutting event with local officials and offer benefits, including networking events and opportunities to email the membership list. Getting people in the door on the first day is important. However, the key to developing a success business is to keep them coming back. Always deliver on the promise and make sure the service is top notch. Encourage your satisfied customers to write reviews on Yelp, Facebook, and other social media outlets. This helps build buzz and creates positive word-of-mouth. Just as importantly, contact unsatisfied customers to find out how you can improve and win back their trust. If someone has posted their grievance on social media, reach out to them politely. Even if that one person cannot be satisfied, if you respond professionally in a public forum, you will win the respect of others who view the post. Be sure to put enough marketing firepower behind the launch. Posters, mailers, advertising via digital and traditional media, and social media outreach are as important now as they have ever been. Keep the foot on the throttle and work hard to build your business. Soon-to-be retirees sometimes start to panic about increased market volatility in the months leading up to the end of their work lives. Here are a few tips on how to help steady your retirement investments from two financial planners.

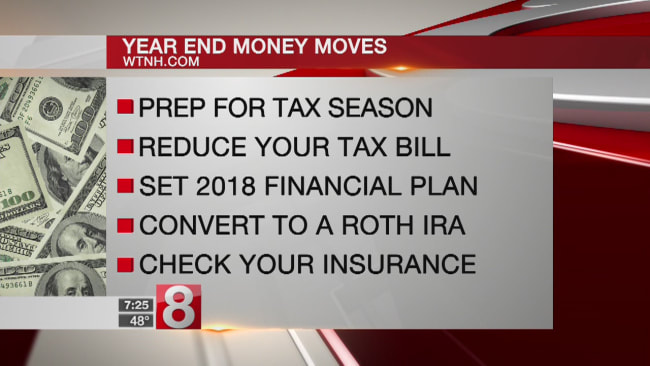

Investors have been shaking off periodic stock-market jolts as the bull marches on, but what about those planning to retire in 2018? Soon-to-be retirees sometimes start to panic about increased market volatility in the months leading up to the end of their work lives, and that’s easy to understand because many of them have read or heard how devastating a negative sequence of returns early on can be for a portfolio. It can be equally nerve-wracking to get too conservative now, knowing the nagging lessons about how portfolios will need to survive longer life expectancies. “I remind clients that retirement is not a finite point in time, it’s the beginning of a 25-plus-year time horizon,” said Harold Evensky, a financial planner and president of Evensky & Katz, a Coral Gables, Florida, wealth-management firm. For those planning to call it quits next year, here are a few steps to help steady the ship from Evensky, who works with individual clients, and Wade Pfau, a professor at the American College of Financial Services, who wrote a book aimed at do-it-yourselfers called “How Much Can I Spend in Retirement? A Guide to Investment-based Retirement Income Strategies.” Create a bucket. Many advisers create complex bucket strategies aimed at locking up specific dollars for specific years in retirement, but that’s not what Evensky advocates. He creates a simple two-bucket approach, putting a single year’s worth of cash reserves into one bucket, with the remainder of retirement investments in the other. The cash-reserves bucket for his clients is invested in short-term bonds, but individuals could explore high-yield savings accounts as well. It helps retirees psychologically to not have to pull grocery money out of the investment portfolio, he said. Focus on a different number. Rather than obsessing over the daily fluctuations of a 401(k) balance as work winds down, spend time verifying the future return assumptions built into an existing nest egg, Evensky said. Currently, he projects that a portfolio invested in 60 percent stocks and 40 percent bonds today will generate just 2.5 percent in real return after taxes, investment costs and inflation. If your return assumptions are too rosy, now’s the time to adjust, he said. Be flexible. Pfau recommends that retirees stay flexible about their withdrawals from retirement accounts, because with a little flexibility, most likely retirees will be able to spend more earlier in retirement than they would if they had to commit to a spending level that won’t change in response to market conditions. He lays out several academic spending strategies from various researchers. One example, from adviser Jonathan Guyton, involves funding a cash-reserve bucket made up of proceeds from rebalancing the portfolio, starting with an initial spending rate of 4 percent of the portfolio and adjusting for inflation thereafter. In negative return years, however, there is no inflation adjustment. And if the withdrawal rate rises by 20 percent above its initial level and life expectancy is still more than 15 years out, spending takes a 10 percent cut.  NEW HAVEN, Conn. (WTNH) – Don’t look now but 2017 is quickly coming to a close! This morning, financial expert Roger Cowen stopped by our studio to talk about 5 smart money moves you can make now that will help your finances in 2018 and beyond.

1. Prep for Tax Season · The tax filing season opens in January, so now is a good time to get ready. · Start by getting organized. · Get folders for all your income, expenses and deductions and your investments. · You can break your deductions down by category; for example, create sections for medical, charity and business. · You can even do a dry run on your taxes so you have a better idea of your tax situation. · It’s a good idea to do this before the end of the year, because you still have time to take action if you choose to. 2. Reduce Your Tax Bill · There are several steps you can take before the end of the year to reduce your tax bill. · Look for any payments you can make early, like your January mortgage payment. If you can make it in December, you can deduct the interest on the current year. · If you have a 401(k) at work, bump up your contributions so more of your income is tax-deferred. · And, of course, be charitable! Donations made to charities in 2017 may be deductible on this year’s taxes. · It can all be confusing, so see a tax professional if you have any questions. 3. Set Your 2018 Financial Plan · Take a comprehensive look at your finances. Did you have any unnecessary expenses in 2017 that you can cut next year? Can you bump up your savings in 2018? · If you don’t have a budget, now is the time to set one! · You may also want to set up a meeting with your financial professional for an annual review, especially if you’re approaching retirement, so you can make any necessary adjustments. 4. Convert to a Roth IRA · You may want to consider converting some of your money from a Traditional IRA into a Roth IRA. · Here’s why: You do not get upfront tax breaks on a Roth IRA, however, your withdrawals are made tax-free as long as you are older than 59 1/2. · But here’s the catch. Roth IRAs are subject to what’s called the 5-year rule; you cannot withdraw your earnings tax-free until five years after the tax year you make your first contribution. · No matter when you make a conversion in 2017, the clock gets set back to January 1st, 2017. · So, if you make a conversion in November or December, it’s like getting a free year! You’ll be able to start withdrawing your earnings tax-free a full year earlier than if you wait until next January. 5. Check Your Insurance · Life insurance always seems to be a daunting topic because we are talking about what happens to your finances if or when you pass away. · Life insurance takes care of your family, helping ensure they will be financially fit even when you are not around. · A good rule of thumb is to get enough coverage for 10 to 15 times your current salary. (Source if you choose to use fact: Forbes) · A life insurance calculator, like the on my website at cowentaxgroup.com can help determine how much coverage you actually need. · Also, Make sure your beneficiaries are up to date. · You may need to make changes if there were any major life changes, like births, deaths, marriages or divorces this year.  Stores are already full of Christmas merchandise and Thanksgiving is days away, so this looks like a good time to share some of my favorite money-saving holiday shopping tips.

In addition to planning ahead, staying on budget, and watching for sales and discounts, there are many opportunities to save money. That's true whether you're buying gifts, or just shopping. Here are some examples: Discount gift cards: Gift cards may be purchased as gifts, but they can also be used to make your own purchases. If you're planning to do a lot of shopping, or dining, at a particular place, check out reputable online resellers of gift cards, and you could get one at a nice discount to face value. Gift cards are just another form of money. If you can get a $100 gift card for $90, you made money. Just make sure to only buy gift cards you'll use. Some discount examples I found: You could buy a $100 gift card for Bass Pro Shops for $88 (cardcash.com), a $75 AutoZone gift card for $67.50 (raise.com), or a $50 P.F. Chang's gift card for $39.75 (cardpool.com). Note that, sometimes, gift cards are sold in electronic versions that can only be used online. Gift card bonuses: Keep an eye out for bonus offers that can multiply your money. Restaurant chains, drug stores and even specialty retailers usually offer deals during the holiday shopping season in which the gift cards you buy may be worth 10 percent to 30 percent more than you paid for them. That's helpful for gift-giving, or to save money at places you regularly shop or dine. Note that a "gift card" does not expire, but a bonus might come in a different form that could have an expiration date. So, you might buy a $50 restaurant gift card that doesn't expire, and also get a $10 "bonus card" with an expiration date. Membership discounts: Say you want to give some movie tickets as gifts. If you're an AAA or AARP member, you can buy them at discounted prices. Credit/debit card cash-back: Many credit and debit cards provide rebates in the form of cash-back, or points. Some offer larger rebates at particular stores, and many offer even larger rebates for online shopping launched from their website's online shopping portal. Get in the habit of launching your online shopping from your credit or debit cards online shopping portal, and you'll save more money. If you're a member of an airline loyalty program with miles or points that can expire, use the airline's shopping portal to shop and you'll reset the expiration date on your mileage program. Valuable protection: Take the time to know the benefits provided by different credit and debit cards, so you'll know the best ones to use. American Express' "purchase protection" will cover a purchase if it's stolen or accidentally broken within 90 days — a great benefit, which I've used in the past, that's particularly helpful for purchases of small electronics that will be gifted to young people. Dropped your new smartphone in a lake? No problem. Citi "price rewind" will let you register a purchase, track the price, and give you money back if better deals turn up. Some cards will automatically extend a warranty, or the time period when returns are allowed. Speaking of credit cards, shoppers are likely to be solicited at checkout, both in person and online, with offers to immediately save money on their purchase by signing up for the store's credit card. Weigh such offers carefully, because store-branded credit cards typically offer lower incentives for signing up, come with fewer benefits and carry high interest rates. Signing up for a credit card shouldn't be an impulse decision. Some store-affiliated cards may make sense if they have no annual fee, you shop there often and they provide ongoing discounts. As with any credit card, store-branded cards are only a good thing for people who avoid interest charges by paying off the balance due each month.  Inequality flourishes everywhere. Just read the front page of The New York Times. The Big Board is still the perfect metaphor for the widening gap between haves and have-nots. Internet properties, Alphabet accepted, still doing twice the market’s 10% gain. Nobody wants small cap goods or even mid cap properties.

Consider Facebook. With a market cap approximating $500 billion, it sells around 7.5 times book value, and at 25 times my estimate of forward 12 months’ earnings. Share based compensation tots up to 25% of earnings and outstanding shares are growing at 1.5%. Facebook holds over $35 billion in cash with $18 billion in goodwill on the balance sheet. To renew itself continuously, R&D runs at 20% of revenues, a most notable number. Apple spends around 5% on R&D. Facebook’s operating margin has expanded to 47% of revenues. This is a work in progress, and I like the vibes. Enormous variance permeates top 100 names in the S&P 500 Index. General Electric, IBM, Coca-Cola and Pfizer are dead paper. But, railroads sell at 20 times next year's earnings power. Schlumberger and Halliburton sell between 30 and 40 times current earnings, as if they're entering an energy super cycle. You can own JPMorgan Chase and Citigroup at 11 times conservative estimates for 2018, a deep market discount, almost 40%. Net, net, corporations like GE, IBM and Coca-Cola seem too big to reinvent themselves. They were the momentum stocks during the sixties. Does anyone but me remember when the Watson’s bet the company (IBM) on their introduction of the 360 Computer? The also-rans remind me of New York State’s northern cities - Buffalo, Utica, even Rochester that flourished when the Erie Canal opened for trade in the 19th century. In the seventies Eastman Kodak was a Nifty fifty stock. I do bet on remakes that could work, starting with AT&T. Last week the market finally liked something about T. Earnings were an upside surprise. The brass ring is the buyout of Time Warner gains approval by yearend, a true media transformation on a piece of paper yielding 5%. I see General Motors as something better than a cyclical metal bender. It's cheap if you give ‘em average earnings power of even $3 a share over 3 years. Currently, the number is $6, the dividend over 4%, at just $1.52. Hopefully, payout is headed to 2 bucks a year or 2 out. I like the way management is playing gin rummy with offshore properties, keeping China and discarding most of Europe and South America. Yes, I know, they needed a $50 billion bailout to survive, but Citigroup was goat meat, too, back in 2009. Never underestimate how long it takes to make things right in the country. Guys in workboots sensed this, buying into the Murphy man’s patter on jobs. How many steelworkers appreciate excess capacity in steel has reigned for over 30 years? Infrastructure spending? No funds coming. Because the country faces deep-seated issues of lopsided income distribution and a progressively defanged, even deranged Oval Office, don't extrapolate more than moderate momentum for GDP. Low interest rates could prevail for years to come. Janet Yellen can't find any inflation using both her hands and feet. Historically speaking, mortgage rates hovering around 4% are a Consumer Reports Best Buy. The Big Board’s largess should prevail, and I'll try hard not to feel guilty about participation. Reciprocal of low interest rates is growth stocks. Alibaba, I love you, but you don't even know it! I'm not giving up on Wall Street getting an increasing share of GDP, but it won't be easy unless “risk on” prevails. Deep seated issues don't fade away. By 2030, the Social Security system falls into negative ground. The push to lower benefits or raise taxes therein hovers out there, maybe in the next Presidential term. They could bump up the qualifying age level a couple of years, and solve it actuarily with a stroke of the pen. My chart on compensation of employees past 3 decades as a percentage of GDP shows a wipeout. Labor’s take contracted from 67% to 57%. How many labor union leaders or even Congressmen have processed this depressing trajectory? Contrapuntally, pressure from the corporate sector to lower their tax rate is very noisy. The Koch brothers openly proclaim they'll spend what it takes to lobby this issue. But, how many Congressmen have reviewed the chart on tax rates for U.S. nonfinancial corporations? Early fifties, we’re talking taxes in upper sixties. Consider, we've been below 30% for much of the past 3 decades. Today, savvy major corporations have whittled down taxes to low-to-mid-twenties. Not much different than the industrial world's norm. Sadly, the Occupy Wall Street crowd waxed vociferous, but shouldered no specific ideology or agenda for change. They should a dug down into the Labor Department's long term stats or perused a dozen proxy statements of tech houses to unveil the scope of corporate management's methodical rapacity blessed by hired consultants. The SEC forever is silent, too busy with insider trading cases so irrelevant to financial markets’ health but do gather headlines. Past 30 years, the middle class lost income share to the top 20%. Income inequality actually increased for the last generation. I define wealthy as the adjective for anyone who doesn't need to work. Their wealth exceeds 30 times middle class income. I'm assuming a realistic after tax income flow of 3.3%, what you'd get on longer maturity tax exempt's. Without a nest egg of $3 million you don't qualify. Sorry! Equity for the middle class largely resides in home ownership. Average equity produces no more than $75,000 net of mortgage debt. Hot real estate locations like Williamsburg in Brooklyn are exceptions. Incidentally, New York City politicians studiously avoided the issue of grossing up for tax purposes huge increases in home values these past 5 decades. Brownstones changing hands today at $2 million carry a tax load around $6,000. Homeowners rejoice, but silently. These homes sold for $15,000 early postwar decade. Never forget, the market is the Great Humbler, smarter than us. My putting bank stocks at a valuation above 60% of the market are dangerous. Citigroup's leveraged exposure of $2.4 trillion in assets is backed by tangible equity of $183 billion. This is the typical bank construct, leveraged at least at 10 to 1. That said, I own Citigroup - big because there're so few others sectors to play for operating leverage. Industrials need a zippy economy, while traditional retailing is assailed by Amazon. Energy quotes are anyone's guess. Cola water has topped out while Procter & Gamble's topline rests sluggish. The existing pharma model of bumping up prices 5% to 10% per annum faces regulatory challenges. I've just eliminated over half the S&P 500’s sector weightings. Internet properties, several now with market capitalizations of $500 billion or more could easily end up at 20% of the Index’s valuation. Forget ExxonMobil. Anyone underweighted in Facebook and Alibaba needs to perform some serious introspection. These stocks are ahead year-to-date at least double the market’s 10% gain. BABA ranges above 50%, and as yet isn’t part of the S&P 500, an ironic twist for my favorite piece of paper. Would an added 1% to S&P's performance. Reciprocally, I'm a player in stocks where I think the consensus is obtuse. Include AT&T, GM and Citigroup, as just too cheap.  During the past few months, I frequently came across story after story about record flows to exchange traded funds (ETFs) that track the S&P 500. Such ETFs include SPY, VOO, and IVV. The main reason for these record flows is obvious -- the U.S. stock markets have been doing very well this past year.

But why are investors particularly flocking to ETFs that merely track an index? There are two reasons. First, these ETFs are pretty cheap. Second, when stock markets are rallying, it seems easy to make money investing. All of a sudden, we may even feel like investment pros. In psychology, the tendency to think we are better than we really are is known as an overconfidence effect. The way this effect can manifest itself in investment decision-making is that we may misattribute our current success in the stock markets to our investing skills, when in fact most of us probably do not know much about investing. A lot of research has been conducted on overconfident investors. In the long run, they do not perform well. Here’s a study on overconfident investors in the United States. Here’s a study that I did on overconfident investors in China. I became curious about these recent ETF flows and so I decided to check out them out for myself. I went to www.etf.com to find information about ETF flows, and I chose to look at flows to the SPY ETF simply because it is probably the most well-known, largest, and oldest ETF that tracks the S&P 500. During the past year, from August 1, 2016, to August 1, 2017, about $16.7 billion flowed into SPY ETFs. I wasn’t sure if this was a large amount, so I kept going backwards, looking at August-to-August annual SPY ETF flows, and discovered that yes, $16.7 billion was a pretty big annual flow, but then I came across the SPY ETF flow from August 2007 to August 2008. It was over $30 billion. Was this an outlier, or was this normal? I continued to go back to 2000, and discovered that no other year’s flow to SPY ETFs came close to the $30 billion flow that occurred from August 2007 to August 2008. I became curious, and so I decided to look at August-to-August annual S&P 500 returns. I discovered that during the year prior to $30 billion flow to SPY ETFs, the S&P 500 had a 13.1% return, which at that point was the largest August-to-August annual S&P 500 return since in the turn of the millennium. What’s my point? Well, it seems that people do gravitate to low-cost ETFs that merely track an index when markets are rallying. But we all know what happened immediately after August 2008 -- the stock markets crashed. By the end of 2008, the S&P 500 fell by over 35 percent since August 1, 2008. The S&P 500 continued to crash in January 2009. So, those many investors that bought $30 billion worth of SPY ETFs lost a lot of money from the market crash if they didn’t immediately sell those ETFs. In fact, if investors purchased a SPY ETF during the market peak in 2008 and finally sold it less than a year later at the market bottom in 2009, then those investors lost about half their money. Yep, half. So, what should investors do when markets are at all-time highs? They should probably be cautious. After all, what goes skyrocketing up can come crashing down. This past year, I have personally witnessed a lot of investors gravitating to tactically managed or actively managed portfolios (in the investments profession, “tactically managed” and “actively managed” are often used interchangeably), instead of to passively managed portfolios or to ETFs that merely track indexes. Why are they doing this? Tactical money managers usually attempt to protect their investors from stock market crashes. So, many investors and their financial advisers who are leery of the current record-high stock market valuations are now searching for “downside protection.” If you are an older investor, someone who is nearing, or is at, retirement, then it may be prudent for you to seek actively managed portfolios that can offer you protection from market downturns. You are now probably wondering if tactical money managers are good at what they do. This Federal Reserve Board study, coauthored with finance professors at the University of California at Irvine, finds that actively managed portfolios can successfully protect their investors from market downturns. Here’s an excerpt from the study: “Using data from 1980-2008, we find that the most active funds outperform the least active ones by 4.5 percent to 6.1 percent per year in down markets after adjusting for risk and expenses… A further investigation of the sources of fund performance suggests that active funds show better stock picking skills in the down markets. The results are robust to different measures of fund activeness and definitions of up and down markets.” So, it seems that on average, active money managers can protect their investors from stock market crashes. By the way, if you’ve read some of my previous Forbes columns, then you know that I am not a fan of mutual funds. I’ve previously described their huge costs, some of which are hidden, and their sneaky behaviors. So, how can you invest in a tactically managed portfolio if you don’t want to invest in a mutual fund? I’ve previously describe the many benefits of separately managed accounts (SMAs). You might think that SMAs are usually reserved for the super-rich. That used to be the case. But today, some investment firms are offering non-wealthy investors the opportunity to invest in SMAs with small account sizes. So you no longer have to be super rich to invest in an SMA. And in case you’re wondering, investors in SMAs did better than mutual funds during the 2008 stock market crash. So, is it time for you to invest in a tactically managed SMA? I don’t know you, so I don’t know. You should talk to your financial adviser. They know your personal financial situation, circumstances, risk-aversion, and goals. And they should know a thing or two about investing. I get similar results if I use January-to-January annual SPY ETFs flows and January-to-January annual S&P 500 returns. I just picked August because that’s the current month, and I wanted to go backwards in one-year increments. It’s no secret that a lot of us want to be rich. After all, who doesn’t want to live a life of leisure in luxury? However, while a lot of us also know that to get there requires a lot of hard work, there are a few other steps you need to become acquainted with.

As there’s no such thing as overnight success, the habits you pick up to grow your wealth are going to require some patience and practice but will be well-worth it in the end. Check them out below: Pick up a side hustle Having a side hustle is going to be one the first ways you can not only gain some extra income but establish yourself for a skill or service. This can mean anything from hosting a drop shipping business to even just running a store on Etsy. Look into what you’re passionate about, and who knows? Maybe it’ll become your full-time gig. Have saving goals As you’ve probably heard 100 times before, saving money is absolutely imperative for financial freedom. However, it’s something that collectively we haven’t been as attuned with, as according to GoBankingRates, a shocking 69 percent of Americans has less than $1,000 in their savings account. Take the time to set aside some of your paychecks as you never know when a rainy day is going to come. Budget for the experiences Another practice of the super wealthy when it comes to savings is setting aside funds for the experiences they want to have. Regardless of income, everyone has some dream vacation or adventure they want to go on, which you shouldn’t feel guilty for wanting to pursue. Whether it is a wine tour through Napa Valley or hiking in Peru, make an effort to put these activities as a priority. Spend money where it counts There are certain events in life that you’re going to want to remember forever, but come with a hefty price tag. Which, if you already know the cost of a wedding or how much a car is going to be, then why try to finagle your way around it? Be honest about the experiences you’ll want to have, and the reward will be much richer. Pay attention to your credit Your credit score is going to be the lifeblood of how much people are going to be willing to lend to you, so it’s best to utilize it wisely. If you’re unsure or don’t know how you’ll get out of the hole, not to worry, as there are plenty of firms out there whose job is to fix credit. Make an effort to develop this, as it will serve you well in the long run. Invest early While a lot of people fear the stock market in thinking it’s a gambling person’s game, it can actually be a great way to get rich slowly. Yet, not everyone sees it this way, because as noted by Gallup, only 52 percent of Americans have money in the market, a record low. Some places to consider include Index Funds, Roth accounts, or even a 401k. Cut out some of the short-term spending Noting our point above on saving for experiences, it’s important to consider the little things you’re spending money on unnecessarily. This includes activities like going out to eat, which according to CNBC, accounts to approximately $140 per month in excess costs. Don’t buy expensive just because you can afford it Do you want to know what the most popular car choice of the wealthy is? According to a study by Experian, Honda, Fords, and Toyotas. The rich don’t always want to show off their wealth, but even more, they view their car as a utility, something that doesn’t need to be excessive. Real estate can have good returns Perhaps one of the soundest investments you can make long-term is with real estate. According to Investopedia, investment in commercial real estate comes around 9.5 percent, with residential around 10.6percent. These figures beat out the S&P 500’s rate at 8.6 percent, even when factoring in recessions. Stay away from loaning money It’s true that there’s such a thing as ‘healthy’ debt, where you’re not biting off more than you can chew, as well as can make payments on-time over the course of a couple of years. However, be very wary of things like credit card debt or loaning money for leisurely activities, as according to NerdWallet, the average credit card debt is $16,883. The interest alone on a balance like that could be crippling, so be mindful of being able to pay every month. Always focus on your passion A big thing any wealthy person will tell you is to focus on your passions, and the rest will come. While it sounds cliche, being excited about going to work every day will seriously increase your drive and hustle. Stay grounded in your decisions Whether it be investing in the stock market, a startup, or even a piece of property, always is mindful of the risk involved. Sure, taking big risks can have big rewards, but also some sizable losses as well. As noted by MarketWatch, those who are after a five-year return fall within a range of +33.35 percent to a -13.22 percent. That’s a pretty wide spread and one that should not be taken lightly. Turn yourself into a business As we mentioned above on your side-hustle, turning yourself into a business/becoming self-employed is one of the most important ways of getting rich. There’s just so much more upside in setting your own price, schedule, and work/life balance. Plus, as the Bureau of Labor Statistic notes, 10 percent of all workers are now self-employed, a number that’s only going to increase steadily.  Success is always associated with wealth. Although you can be successful without becoming wealthy, most people who struggle financially consider financial independence as success. If you really want to succeed, clean up your finances and make an educated decision as to what kind of loan will take you on that path. Considering personal loans also known as signature loans, like signature. Loan recommends, can lead you to that goal of reaching financial success.

On the other hand, success is built on specific habits that are common traits of many self-made wealthy individuals. Regardless of your financial status today, you are likely to become wealthy and successful if you possess the right qualities. If you don’t have these qualities yet, it’s time you start developing them now. Today, we will be going over these habits that foster wealth and success. Let’s get started! 1. Wealthy People Know What They Want Just like architects, wealthy people have their own blueprint of their future. They know exactly what they want, so they know what they need. They plan their goals carefully. Once they are in the building process, they do not compromise their plans. They are open-minded, but they are determined to prove they’re on the right track. 2. Wealthy People Never Surrender When they are down, the more they become eager to move forward because they know that moving forward is the only direction left. That’s how they think, so they do not give up easily on something, especially on achieving a goal. 3. Wealthy People Are Less Talkative but More Action-Oriented Most unsuccessful people are the ones who have a lot to say. They are good at reasoning out. These are the people who keep on complaining about many things. Meanwhile, wealthy people talk less as they keep thoughts to themselves. They want their results to speak louder than what they would say. They will not tell you “this can be done.” Instead, they will just do it and show you how. 4. Wealthy People Avoid Negative People Wealthy people are not interested in getting along with negative people. They are not comfortable hearing expressions, like “I hope so,” “That’s impossible,” “I am not sure,” and so on. The people they want to be around are positive people who are passionate and enthusiastic about what they do. 5. Wealthy People Do Not Procrastinate It’s no secret to everyone that procrastination is one of the many obstacles toward success. For wealthy people, time is of the essence as they consider time as a precious commodity. Instead, they increase time’s value through organization so that it’s properly utilized. This is why their own rate, they set for themselves is much higher than other people in the workplace. 6. Wealthy People Work Hard Everybody knows that working hard is the key ingredient to success; however, many people simply don’t do it in reality. This habit is not a secret as all you have to do is apply it in business. Wealthy people work hard, but they schedule out their time accordingly. 7. Wealthy People strive to be Frugal Wealthy people put a large portion of their money into some type of investment in order to make more. They tend to be frugal with their money as they use wisely on specific purchases. Wealthy people tend to also make budgets and stick to them in order to succeed. Final Thoughts To foster wealth and success you have to have the right mindset. Following the habits that have been outlined today will get you started on the right path. Which processes will you apply in your life in order to achieve wealth and success?  They say you have to spend money to make money, and this is especially true when you're seeking financial guidance. Financial advisors are well-paid for their in-depth expertise and often help their clients through decisions like investing, retirement planning and long-term savings plans.

Although it's still wise to consult a professional before any major investments, you can educate yourself enough to confidently make your own personal financial choices without the help of a professional. Nine members of the Forbes Finance Council shared their best do-it-yourself tips for individual investors looking to better manage their finances. 1. Invest for the long term. The lure of a quick buck can guide investors to make certain investing decisions. But, unless you're a day trader, a long-term strategy is the best way to protect your assets while ensuring ROI in the long run. The market will fluctuate over time, but history shows that it tends to go up in the long run, so looking to the future will keep an investment plan focused and profitable. - Sari Holtz, DailyForex 2. Open a Roth IRA. If you're just getting started with investing, a Roth IRA can be a great way to start. Since it is a tax-advantaged investment, it allows your wealth to grow and compound tax-free. Your investments are initially taxed, so you can make withdrawals tax-free in retirement. And, you will typically have access to a wider range of investment opportunities with a Roth IRA than you would with a 401(k). - Elle Kaplan, LexION Capital 3. Don't follow fads. I believe that everyone can be successful in managing their own finances as long as they are well-informed. A common mistake I see individuals making is investing based on a trend or fad instead of research. Read everything you can get your hands on, and question unproven assumptions. - Mahati Mukkamala, Klaviyo 4. Purchase indexed annuities. Sold by insurance companies, indexed annuities offer a way to participate in stock market gains while limiting downside risk. When the market is climbing, you'll share in the returns, but you'll be protected from losses by a guaranteed return even when stocks fall. The guaranteed return means that even inexperienced investors can participate without big risk. - Danielle Kunkle, Boomer Benefits 5. Take advantage of money management apps. I personally manage my own money and regularly use apps like Mint and Robinhood. Mint keeps my personal finances in check, and I invest through Robinhood. Both have extremely low fees and are easy to use. Money management and investing aren't just for the pros anymore; the fintech trend has resulted in new resources and apps at your fingertips. - Rachel Carpenter, Intrinio 6. Invest in a lifecycle fund. Lifecycle funds require very little work on your part. Unless you really know exactly what you’re doing, it’s the best way to go. As long as you keep stashing money away, it should keep working for you. - Ismael Wrixen, FE International 7. Look into low-cost index funds. Paying investment professionals to manage your portfolio can often cost you a lot of money unnecessarily. When you add in the cost of actively managed investment options, the average managed portfolio will underperform the market. The best investment most people can make, whether they're wealthy or just have a few hundred dollars to invest is a low-cost index fund. - Paul Paradis, Sezzle Forbes Finance Council is an invitation-only organization for executives in successful accounting, financial planning and wealth management firms. Do I qualify? 8. Be resourceful with technology. In the technological era, everyone can be successful with their finances without professional interference. Take advantage of the resources at your disposal. Thousands of apps and websites can aid in the investment process. Record keeping is a must-do, and it’s the only true way to monitor and adjust for proper spending. - Ibrahim AlHusseini, The Husseini Group 9. Budget, budget, budget. Know how much you spend monthly and what you spend it on. If you're able save $500 to $1,000 each month and place it into an investment account, you will witness the phenomenon of compounding interest first hand. Making this systematic is the key to it actually happening. Don't look at saving money as an idea but as a way of life. You will thank yourself later. - Lance Scott, Bay Harbor Wealth Management |

RSS フィード

RSS フィード